Back to myNiagaraOnline

Back to myNiagaraOnline

A way to enhance a life insurance policy by incorporating an additional component.

One solution often considered by individuals looking to integrate an additional component into their protection strategy is a type of product known as “participating” life insurance.

Here is a brief overview.

Enhanced life insurance

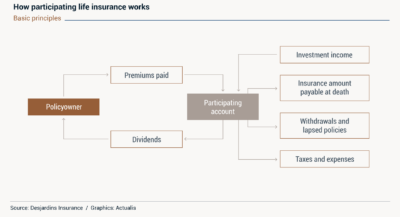

Participating life insurance has two components. The first includes all of the policy’s guaranteed values: the amount of premiums paid by the insured (which are set for the life of the contract), certain cash values and, of course, the value of the death benefit to be paid. The second is the participating component. It does not come with a guarantee, but does allow the policyowner to “participate” in the returns provided by the policy when the insurer invests the proceeds in the market.

The following diagram illustrates the basic principle. As we can see, in return for the premiums paid, the policyowner could receive “dividends” arising from investment income, net of the insurer’s obligations (death benefit payments, expenses, taxes, etc.). These dividends are paid out of a “participating account,” which is a pool of participating policyowners. This account is segregated within the insurer’s overall accounting and any net surpluses generated are intended only for that specific pool of policyowners.

How dividends are distributed

The mechanics of participating life insurance may vary depending on the policy, the options and the insurer. As a general rule, the policyowner will be paid a dividend in each year that the participating account outperforms the assumptions used to determine the guaranteed values. These dividends are not guaranteed, but once they have been paid, they are vested with the policyowner.

Depending on the policy and the options chosen by the policyowner, the dividends paid by the participating component can be used in various ways: for example, to purchase more whole life insurance, take out additional insurance, be applied against the policy premiums (in which case the dividends might be tax free), provide a cash rebate, or be invested in an interest-bearing deposit account.

Who is participating life insurance for?

Participating life insurance generally attracts individuals who wish to acquire life insurance with guaranteed values (especially premiums and cash values) and have additional cash resources available after their coverage needs have been met. The participating component allows them to use these cash resources to enhance their estate and their retirement income, cover inflation risk and provide additional asset diversification. As with any life insurance, tax advantages may also be possible. This product is particularly popular with business owners.

However, this insurance and investment solution may initially seem complex and bring an element of risk into the strategy: in exchange for “participating” in returns, policyowners also agree to share in the insurer’s investment risk that makes those potential returns possible.

Your financial services professional will be able to provide you with information and help decide whether this might be a good choice for you.